• SPACs offer many advantages over IPOs or raising more private capital

• Strategic venture investors have several tools to mitigate the risks and add value

The spring selloff of SPAC stocks has prompted concern about the future of this complex merger/IPO mechanism. But recent trends only reinforce the importance of understanding how valuations are set in SPAC deals, which we believe will continue to reshape the market for venture capital exits.

Special purpose acquisition companies (SPACs) have accelerated the path to public markets for privately held companies. For years, startups stayed private for longer, backed by massive capital injections from megafunds. Now, the road to public markets has been reopened by SPACs, shell companies established with the sole purpose of raising money through an IPO to eventually acquire another company. SPACS have become a legitimate and attractive option for company founders and investors alike.

Still, many questions deserve attention. Why should startups pursue a SPAC buyer? Does the valuation process work without traditional IPO gatekeepers? And how can you reduce risks for investors after the target company is acquired and listed? By taking a closer look at the dynamics of these deals, investors can gain confidence in SPACs as a powerful vehicle for unlocking value of promising companies.

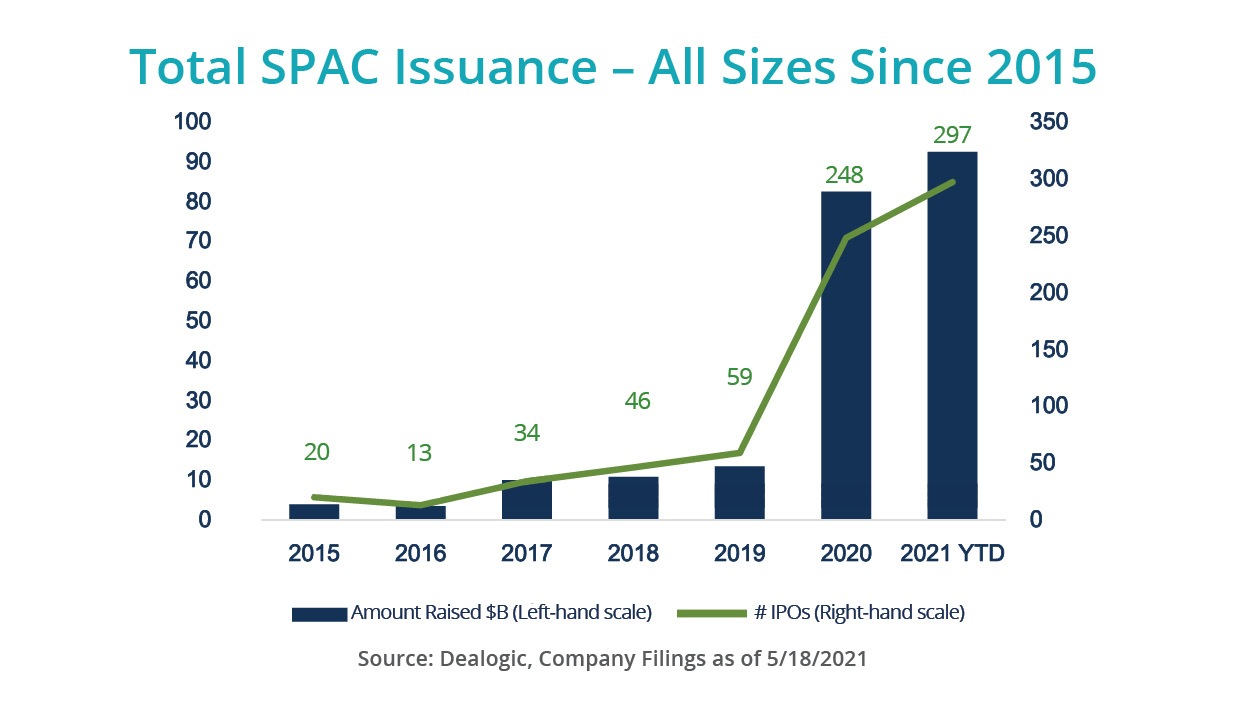

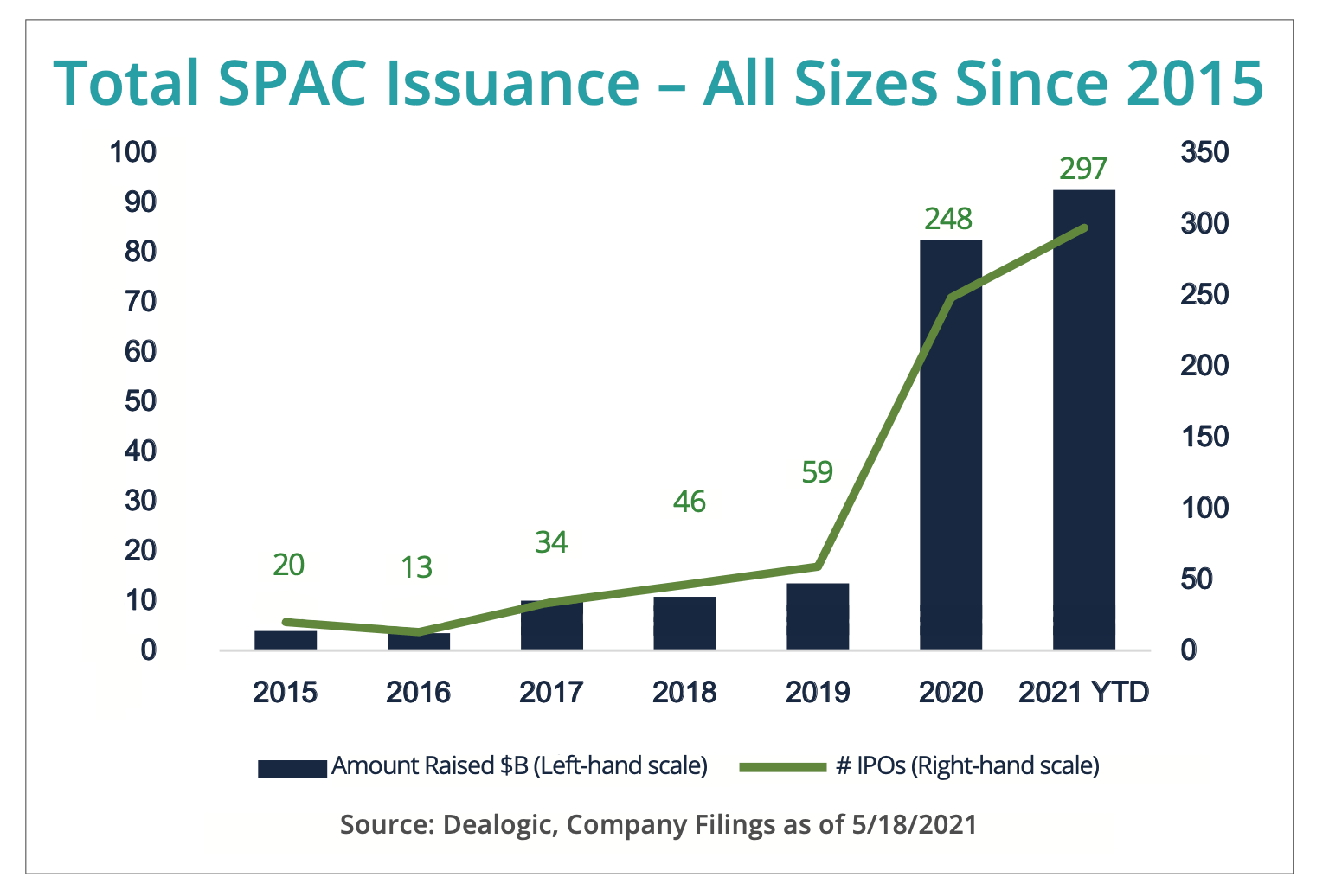

SPACs have been around since the early 1990s but have only recently gone mainstream. In the first quarter of 2021, SPACs raised $92.5 billion in 297 listings—more than all of last year and nearly seven times the value of issuance in 2019. Target companies span an array of industries from technology to finance to healthcare. Our research suggests 96% of SPACs successfully complete a takeover, based on acquisitions completed and pending as a percentage of SPACs raised that are no longer actively looking for targets. For startups, SPACs are changing the balance between staying private for longer and public market exits, in our view.

Pursuing a SPAC Buyer

Startups have discovered several advantages over a traditional IPO process or taking on additional late-stage private capital. First, a SPAC transaction can potentially be achieved faster—and with more price certainty—than an IPO. SPAC deals are less sensitive to market conditions than IPOs, where pricing can be undermined by market volatility. And target companies aren’t shackled by regulations. They can provide much more detail about their business and investment plans, including detailed financial forecasts and forward-looking statements that the SEC doesn’t allow in an IPO prospectus. That said, going public via a SPAC carries all the obligations of a publicly traded company. For example, once listed, the target company is subject to rigorous corporate governance requirements. Companies that aren’t mature enough to meet these conditions should be discouraged from seeking a SPAC buyer.

Target companies should also have a clear strategic rationale for seeking a SPAC buyer in the first place. In our view, SPACs aren’t just an exit vehicle to pay off founders and investors, but rather a source of funding for future business growth and M&A opportunities. So SPAC sponsors must have industry expertise aligned with the target, as well as similar ambitions and a compatible culture. If they can’t get along, the SPAC match won’t be made in heaven.

The Valuation Process

When all the strategic elements fit, valuing the target is the next hurdle to a successful SPAC marriage. Here, too, SPACs have become a catalyst for dramatic change in the marketplace.

In the past, investment bankers were Wall Street’s gatekeepers. They would decide whether a company was ripe to go public, and if so, at what price. There’s always been some tension in the IPO valuation process between institutional investors on one side, and VC investors and the private company on the other. Often, companies were left wondering how much money the investment bank left on the table to woo IPO investors—and to turn a profit for itself. SPACs have disrupted this model. Sponsors of SPACs—experienced businessmen and investors themselves—have taken control of the valuation process. Drawing on their deep understanding of the target company’s business, competitive advantages and growth potential, they determine a price.

Critics argue that this approach is flawed. Without investment banks in the picture, who do the SPAC sponsors serve? Perhaps the founders and venture investors are disadvantaged without a price discovery process or fairness report, typical of IPOs and M&As respectively.

We disagree. In our view, SPAC deals have a robust valuation process, by virtue of the private investor in public equity mechanism, commonly known as the PIPE. Almost every SPAC deal today includes PIPE investors, ideally top-caliber institutional investors who conduct rigorous due diligence. Their participation is a valuation sanity check which provides a strong signal that the price is right.

Reducing the Risks

Getting the valuation right is critical to success. While target company founders often crave an inflated initial valuation, that’s just a tombstone. The real test after the de-SPAC process—when the target becomes publicly traded—is how the shares perform in the months ahead.

Regulators are closely monitoring SPAC trends and will intervene as they feel needed. In April, for example, the SEC raised concerns about the accounting treatment of warrants received by PIPE and sponsor group investors. We don’t see this as a showstopper, rather, as a technical issue that will be addressed in the transaction valuation of the SPAC and the ratio of shares allocated to the target company, sponsors and PIPE investors.

Much has been written about the risks to investors. Academic studies have warned of dilution hazards inherent to the highly complex SPAC deal structure. High profile failures and the increasing participation of retail investors in SPACs have triggered calls for tighter regulatory scrutiny.

Many of these concerns don’t really pertain to venture investors in the target company. Dilution risks are borne mostly by the SPAC sponsors. Poor performance after the de-SPAC generally stems from deals that weren’t valued right.

Strategic venture investors have several tools to mitigate the risks and add value. First, investors with board seats can proactively help steer a target company toward the right strategic SPAC for future growth. Second, investors can apply in-house expertise to influence the valuation process in the right direction. Third, we can scrutinize the PIPE to determine whether these investors are committed for the long-term and are unlikely to redeem shares quickly post de-SPAC, which could destabilize the price in the open market. Finally, venture investors can help secure access to the PIPE for clients, increasing their stake in the new public company at a potentially attractive price.

Recent weeks have seen some changes in the SPAC market, highlighting the volatility of this new asset class. SPACs seeking to de-SPAC have encountered challenges in raising PIPEs to compliment the capital for a transaction and confirm the transaction terms.

While this standoff has slowed the completion of transactions, we expect this will be resolved due to the large amounts of capital in trust and the number of announced potential companies aiming to de-SPAC. Potential solutions to the slowdown may see shifts in ownership of the SPAC between the sponsors and PIPE financiers. Another fallback position for companies considering or in process of merging with a SPAC could be for them to seek a straight IPO or listing of their company, taking advantage of their updated financials and availability of materials.

Both options lead us to conclude that the trend of SPACs and companies listing on the public markets will continue through 2021 and beyond. With a keen grasp of the strategic rationale, valuation process and potential risks, investors can tap this newly popular source of liquidity to generate enhanced returns by supporting the next stage of growth for portfolio companies.

First published in Prospective, quarterly perspectives on VC, technology and market trends published by OurCrowd. To join the Prospective mailing list, email prospective@ourcrowd.com.

Related: