The following is an excerpt from the OurNetwork Q2 Innovation Report, downloadable here.

Amazon and Whole Foods: What We Learned About Corporate Innovation

By Yehoshua Zlotogorski

When does staying ahead of your competitors require inventing something new and when is M&A enough? Where do we draw the line between technological innovation and business model innovation? Let’s take a look through the lens of the recent Amazon-Whole Foods (WFM) tie in, and shed some new light on this acquisition.

It’s all about the kale chips

Let’s start with the why. Before jumping into what I think is the real reason (spoiler alert), I’ll touch on the mainstream narrative I’ve read over and over, which has mainly been about “Amazon eating the world” and how Amazon is playing offense in same-day delivery with this acquisition. WFM gives Amazon two main things: real estate in populated areas and a grocery arm large enough to supply Amazon Fresh. The real estate play has clear synergies: Amazon now has 400 stores located in prime (pun intended) locations, able to serve as hubs for other Prime items. Building out fulfillment centers has been a challenge for Amazon over the past several years, and with one fell swoop, they now have 400 such locations.

The grocery angle comes down to one sentence: As Amazon did to books (and everything else), now so with groceries. By leveraging their superior logistics, customer data, Prime and AI (of course), Amazon will now dominate our everyday shopping experience. This was clearly seen in the public markets’ reaction to the buyout: while AMZN & WFM both rocketed, other food retailers plummeted, namely Safeway, Kroger, Costco, Walmart, Target etc.

There is no doubt that Amazon is a fantastic company, and Jeff Bezos one of the premier CEOs of our age, but is it really that simple? Can Amazon just leverage WFM’s 400 retail locations and win with Prime? No. Integrating a $13.7 billion company isn’t that easy. This is the biggest acquisition Amazon has ever made, and by far. Leveraging WFM’s for same day delivery isn’t that simple – systems have to be synchronized, locations have to be optimized, inside for storage, accessibility and turnover, and outside for delivery and logistics. Transforming a supermarket into a fulfillment center just isn’t that easy.

If a physical foot print was all Amazon was looking for, wouldn’t it be simpler to just purchase space? That would give them the flexibility to choose the right locations to fit their needs.

Size Matters

It’s clear that this purchase revolves around food delivery. But is Amazon really playing offense? For a while now Amazon has had Amazon Fresh, their grocery delivery service, but it’s been struggling to get off the ground. So what are they looking for with the acquisition of WFM? Here is where leveraging WFM size really matters.

The reason is simple – fresh food is a drastically different business than every other item Amazon deals with. Whereas books, clothes, consumer electronics and content have no expiration date, fresh food does. This one key difference is what has caused Amazon so much trouble in building out Amazon Fresh. In a non-perishable product category, items can wait in the warehouse, and other than maintenance costs, products can be stored until shipped. This enabled Amazon to purchase a large stock and sell at whichever pace the market supplied.

With food, this simply isn’t the case. If not purchased, perishables (as their name so aptly describes) – perish. Demand can’t be built out at a leisurely pace; rather, it must reach a critical point from the start. Otherwise, food remains on the shelf and spoils, causing losses. On the flip side, without being able to trust that the produce will be bought, it’s difficult to invest in variety and SKU’s, leading to a poor consumer experience, which leads back to a lack of consumer demand. It’s a vicious cycle.

“Until now, grocery stores who have resisted giving their customers the ability to shop from outside the store – via online and mobile – have merely been falling behind their more progressive peers. With Amazon now directly in the grocery space, stores who continue to ignore their customer desires will be roadkill within five years.” Jon Polin, Storepower, CEO (Storepower is assisting leading brands and supermarkets, such as Fairway.)

In order to achieve the necessary offerings and variety in groceries to supply Prime consumers with a good experience, scale was needed, and quickly. This is why Amazon had to buy a supermarket chain. WFM made the most sense on a lot of metrics – customer overlap and service, prime locations and importantly – size, which was juuust right.

Why Whole Foods Market?

WFM is small enough for Amazon to acquire, yet still gives Amazon the necessary scale. Their locations and customer segment correlate well with Prime users. Most importantly, their consumer experience can be a key edge in online groceries. The mistrust in a courier choosing our fresh produce, or the “I want to choose my family’s tomatoes” mentality has been a barrier to grocery delivery. What better brand to tackle this than ‘Whole Foods – America’s Healthiest Grocery Store’? WFM commits to the highest quality produce and their employees usually know more about the 24 ways to pick fresh river salmon than we do. The WFM brand coupled with Prime prices could go a long way in creating trust in produce delivery.

Defense! Defense!

Why is food delivery so important? Margins are low (although so are Amazon’s in general), products are commoditized and fresh food delivery is yet to be done profitably. The reason is that Amazon needs food delivery to defend its leadership. In other words – Amazon is playing defense.

Today’s consumers are different than yesteryear’s. Everything has to be at the touch of their fingers, any place, any time. UX is key, ease of use paramount. This has always been Amazon’s edge: not the individual products they sell, but rather the whole bundle. Without having a full suite of offerings, Amazon could easily lose out on the marginal purchases that consumers make. Prime users want everything in Amazon’s app whether it be content, music, their new PC or the weekend groceries. Amazon has realized this key functionality and is determined to supply it at the highest level. The only way to do this was to purchase the size and scale that WFM could provide.

But why are they so worried about defense and their consumers? Prime is inching closer every day to becoming the U.S.A’s dominant club membership (Costco is still leading with some 85+ million members). Who could realistically take their crown?

Winds of Change

Here’s where Walmart and Target enter the picture. As unlikely as it sounds, Amazon is worried about these two stalwarts of the U.S “old economy.” Both have the same thing going for them – they’re already well situated in every critical geography, with locations within five miles of most Americans. Their supply chains are built out and ready for scale. The only thing that’s been missing has been the technological edge to dominate in e-commerce, logistics, consumer preferences and AI.

But all of that might be changing. Both of these big boys, and others, know they’re behind and are adamant about catching up. Target announced earlier this year that it will be spending $7 billion on adapting to the new era of retail. Walmart has gone on a buying spree rarely seen among large corporations – over $3.5 billion in the past year alone, and has also launched their own accelerator last year. Most of the old school of retailers are making a push here, and results are starting to take shape.

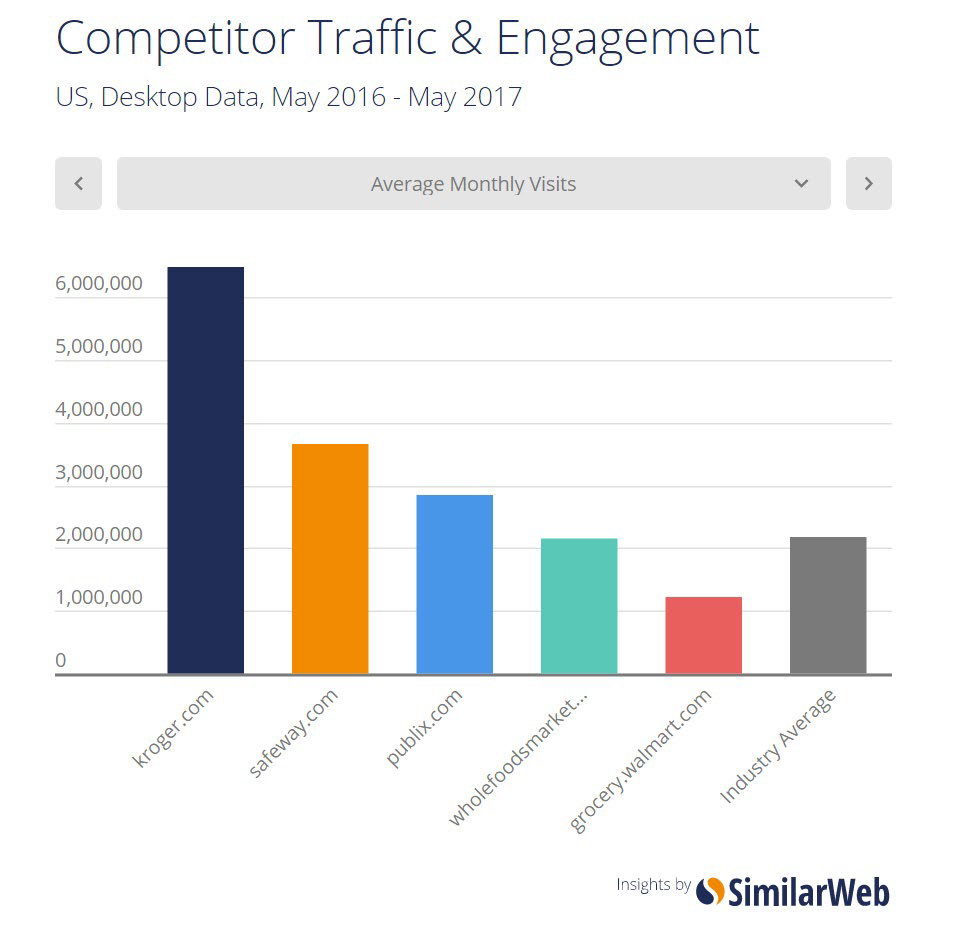

Kroger clearly leads the pack in web page visits to their online grocery shopping site.

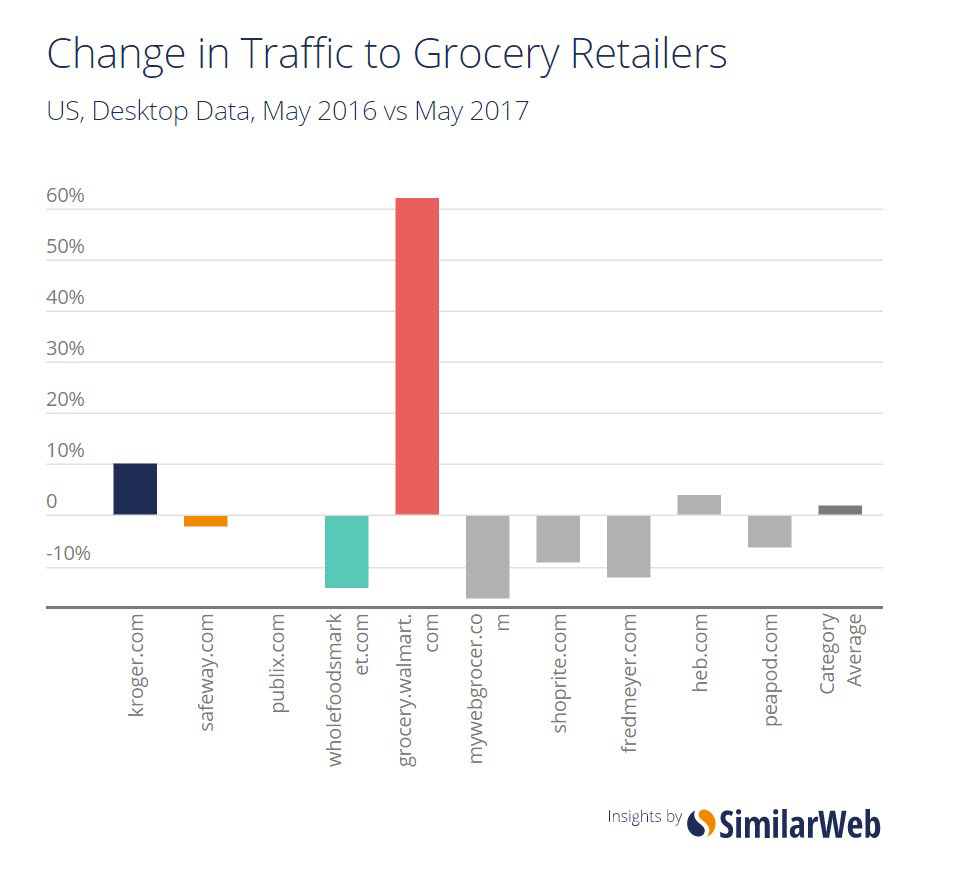

Whereas Walmart’s pace of growth has been the fastest.

Target has also grown its e-commerce rapidly, compounding at a rate of over 30% in past three years. Everyone is coming after Amazon. But so what? Amazon has been so dominant for so long. Do they really have the tools to win?

I believe the answer is yes.

The race is far from over, but today, the tools exist for large retailers to catch up. Whether in Silicon Valley, Tel Aviv, London or Paris, startup ecosystems are flourishing. Innovation abounds, and we are only just getting started. Young companies are tackling issues that only several years ago seemed insurmountable: Blockchain will drastically improve supply chains. Marketplaces and fleet utilization are enabling same day, on demand delivery even without massive scale. Clothes can be tried on remotely and one click checkout is on its way to becoming the norm. Many of the edges that Amazon has long held via its scale and sophistication, namely, a superior supply chain, e-commerce platform and consumer experience might soon be adapted and adopted by legacy retailers learning how to integrate outside innovation. Amazon is seeing this, and they’re moving quickly to protect their moat.

So, does staying ahead of your competition require the invention of something new? Amazon sure doesn’t think so. Neither do Walmart or Target. The main lesson from this acquisition is that properly integrating outside innovation can work. That corporations properly partnering with the right companies at the right time are a real challenge to Amazon, one of the most innovative companies of our age.

Interested in more content like this? Download the Innovation Report here.