The Evolution of the Internet

In order to understand the value proposition of blockchain, it’s important to understand how the internet has evolved from the perspective of the consumer.

At first, the internet was a giant source of information. Aptly dubbed the “information superhighway,” instead of driving to a library, picking up a newspaper, or flying to a museum, people could just “go online” and read about it. With more information at their fingertips, more people got involved. Individuals started adding opinion pieces like blogs and social media to the mix, thereby expanding and adding more and more information to the network.

The next iteration of the internet was applying “not having to go to a library” to not having to visit a store—leading to the birth of the e-commerce site. Instead of driving to the supermarket or clothing store, consumers could order items from the comfort of their own home (and later smartphone/IoT devices).

Although transactions through e-commerce or financial platforms are done online, in terms or services bought, sold, or transferred are digital representations of something physical. A person could go to his or her bank, withdraw $50K in cash, and drop it off at the car dealer for their car- or could send a wire transfer through his or her online banking portal. The same goes for stocks, groceries, movies/TV shows, or anything else purchased online.

In 1999, economist Milton Friedman posited a new idea with regard to the evolution of the internet. Freidman spoke about how the growth of the internet would allow for more deregulation and less government oversight, but there was still one thing missing.

“The one thing that’s missing, but will soon be developed, is a reliable e-cash, a method whereby on the Internet you can transfer funds from A to B, without A knowing B or B knowing A.”[1]

In other words, Friedman suggested the next phase of the internet would evolve from a digital representation of something physical, to a digital store of value that exists exclusively on the internet, like an eCoin.

Roadblocks: Trust and Scarcity

Though Friedman suggested the creation of an eCoin in 1999, there still roadblocks that had to be navigated before a viable digital currency could be released.

When creating a store of value, there are two main challenges. In normal transactions, a central party (bank, credit card, etc.) serves as the guarantor for the transaction. This is known as a centralized network and can be seen in the image below.

But the internet isn’t a central system, rather it’s decentralized. There isn’t a single overseer of the internet, it’s instead a collection of server hubs storing and exchanging data. In a decentralized system, there is no central party, so the issue of trust needs to be resolved.

Figure 1: Graphic Representation of Networks[2]

Another hindrance is creating scarcity, or a limited supply. If a product has the potential for an infinite supply, then the item becomes hyperinflated and loses most or all of its value. Also known as “double spending,” a buyer has no way to authenticate that they are the exclusive owner of a digital asset or if that eCoin has been sent to someone else.

Bitcoin: The Genesis of Blockchain

Nearly a decade after Friedman’s prediction, the anonymous Satoshi Nakamoto published his solution to solving digital scarcity and trust in the whitepaper “Bitcoin: A Peer-to-Peer Electronic Cash System.”[3] The theory behind Nakamoto’s solution is simple yet elegant. He describes the creation of a public record of transactions similar to an accounting ledger. When all transactions are public, then there’s a record to see if a fraudster has transferred their eCoin to someone else already. In Nakamoto’s words:

“…transactions must be publicly announced, and we need a system for participants to agree on a single history of the order in which they were received. The payee needs proof that at the time of each transaction, the majority of nodes agreed it was the first received.”[4]

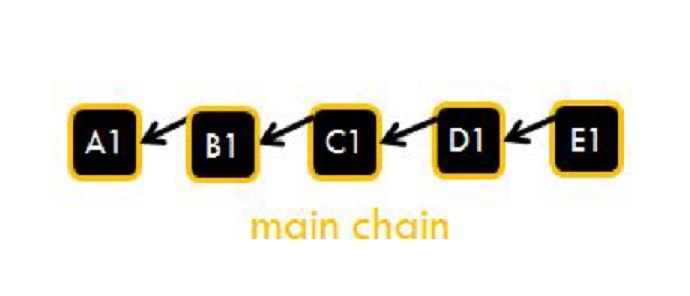

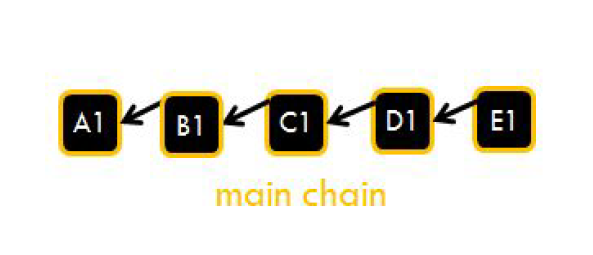

Figure 2: Simple View of Blockchain Block Order

Nakamoto dubbed the public record described as a blockchain. Simply, when A wants to transfer an eCoin to B, A sends, or broadcasts, the transaction to the blockchain network. The blockchain network is made up of nodes, or people controlling servers that have a full history of all transaction on that blockchain, in this case the eCoin blockchain. These nodes are able to authenticate that funds have not been sent to someone else and are in fact controlled by A (thereby solving the trust issue). The nodes can, if they would like, also authenticate the transaction sent from A to B, affirming funds were in A’s possession are now controlled by B. There people are referred to as miners. Miners take the transaction A sent to B and combine them with other transactions to form a set of transactions, known as a block. A miner places the block of transactions after the previous block, thereby creating a chain. The process of a miner authenticating transactions is known as proof of work, or PoW. A simplified view of the process can be seen in Figure 1. Block A comes first, with miners attaching subsequent blocks (B through E) to it as time goes on and more transactions are created.

This chain of transactions (which each node has on record) is known as a blockchain. As a reward for authenticating transactions, miners receive a payout of whatever the native currency is or a fee paid out by individuals wishing to send a transaction.

It’s important to note that anyone can be a node or a miner, making the system distributed, as seen for the image above. This is why blockchain is known as a distributed ledger– all nodes have equal weight and are interconnected.

Another way to understand the process is to compare proof of work to how Visa works. Visa is a centralized network, so anytime a credit card is swiped, Visa has all the information about the buyer in their database. This includes their credit line, payment history, personal information, and more, and allows Visa to give an answer as to whether or not the transaction should be processed or rejected.

In a blockchain, an individual sends a transaction to the network, and instead of a central party validating and processing it, any miner can. The miner automatically at the record of transactions stored on its server to see if funds have been double spent. If everything checks out, the miner authenticates the transaction, which stays pending until a pre-specified time elapses.

The distributed network layout also provides increased security. A centralized network like Visa has a single node which authenticates and holds all transactions. All a hacker or fraudster would have to do is attack the single node and the network would be compromised.

With distributed or decentralized networks, there are multiple nodes holding information and authenticating transactions. A fraudster would have to “fight” against the authenticating process, or all the honest nodes in the system to get transactions through. The fraudster would “win” if he/she has a majority of nodes being fraudulent, known as a 51% attack. In the case of some of the largest public blockchains, can have above 10K[5] and even 20K[6] nodes, making a 51% attack extremely difficult.

Nakamoto decided to create an experimental store of value using his blockchain invention and created a digital currency, or cryptocurrency, called Bitcoin. He distributed funds to anyone who wanted to experiment using the technology. He also wrote into the computer code behind Bitcoin a limited supply of coins that could be created, thereby creating digital scarcity.

Although Nakamoto’s initial application dealt strictly with a cryptocurrency, anything of value can be transferred via a blockchain. For example, music, video, or image files can be stored on a blockchain and bought, sold, or transferred, with all transactions public. The same can be applied to stocks or any other digital asset, whether it exists in the physical or digital world.

Ethereum: A Decentralized Platform

Five years after Nakamoto published the Bitcoin white paper, a miner by the name of Vitalik Buterin published his vision of blockchain. Entitled “Ethereum: The Ultimate Smart Contract and Decentralized Application Platform,”[7] Buterin builds on top of Nakamoto to create something entirely new. In Buterin’s words:

“The intent of Ethereum is to create an alternative protocol for building decentralized applications, providing a different set of tradeoffs that we believe will be very useful for a large class of decentralized applications…Ethereum does this by building what is essentially the ultimate abstract foundational layer: a blockchain with a built-in Turing-complete programming language, allowing anyone to write smart contracts and decentralized applications where they can create their own arbitrary rules for ownership, transaction formats, and state transition functions.”[8]

Ethereum, in essence, allows for the creation of smart contracts on top of a blockchain. A simple way to understand smart contracts is the sale of a home via an escrow account. A wants to buy a house from B, but he wants the funds to sit in an escrow account until he’s done a title check, inspected the home, and any other precursor to taking full ownership.

A sends funds to a smart contract account, and B sends the house deed to the same smart contract account. The smart contract automatically observes the terms specified (the conditions described above in our case) have been met or not. If at any point the smart contract is breached, funds go back to their respective parties. If all requirements are fulfilled, then the exchange is automatically executed, and A takes ownership of the home.[9]

Ethereum allows anyone to build a smart contract based application, known as distributed apps or dApps, on its blockchain. These dApps can be anything, from casinos to purchasing cloud storage, from real estate transactions described above to buying computing power- the possibilities are endless.

A comparison can be made between the evolution of cell phones, an example Buterin himself uses. Cell phones started as a mobile way to communicate with one another. This is akin to sending Bitcoin payment transactions over a blockchain. Then the smartphone came out, which includes internet access, text messaging, and an infinite number of apps. The smartphone is like Ethereum, where functions other than sending payments (like reserving cloud storage, taking part in an auction, creating an organization, etc.) are available on top of the platform.

Ethereum created a cryptocurrency for its platform, known as ether, but the functionality is different than that of Bitcoin. Ethereum serves as a store of value in the same way Bitcoin does but also serves as a way of triggering smart contacts. Ether is used as gas the same way a car uses gas, a means of triggering an event. So, when interacting with any smart contract built upon Ethereum, a little bit of ether needs to be sent along with other digital assets.

There’s a lot more to discuss, but that’s a brief overview of blockchain and cryptocurrencies. We’re going to be discussing blockchain on a deeper level at the OurCrowd Investor Summit. Looking forward to seeing you there in person or virtually.

———

[1] Full video: https://www.youtube.com/watch?v=leqjwiQidlk, https://www.coindesk.com/economist-milton-friedman-predicted-bitcoin/

[2] https://blog.synereo.com/2017/03/20/epiphytian-decentralization-a-new-business-model-for-ugc-publishing/

[3] https://bitcoin.org/bitcoin.pdf

[4] Ibid, p. 2

[6] https://www.ethernodes.org/network/1

[7] https://github.com/ethereum/wiki/wiki/Ethereum-White-Paper

[8] ibid

[9] It should be noted that although smart contacts are called “smart,” they are only as effective as the terms placed on them. If an individual enters into a smart contract without understanding terms is the same as someone who signs a contract without reading it.

![[Codility in TechCrunch] 3 strategies to make adopting new HR tech easier for hiring managers](https://blog.ourcrowd.com/wp-content/themes/Extra/images/post-format-thumb-text.svg)